Global market fundamentals remain mostly supportive of prices, as milk production in the northern hemisphere goes through its peak, while the improving COVID situation allows for significant re-opening of food service channels.

With the arrival of some warmer weather, EU milk output is expected to grow at little faster yet persistent demand for cheese has been limiting the availability of milk being sent to driers. The onset of summer – expected be warmer than usual – will lift demand for cream and sustain tight supply of butter.

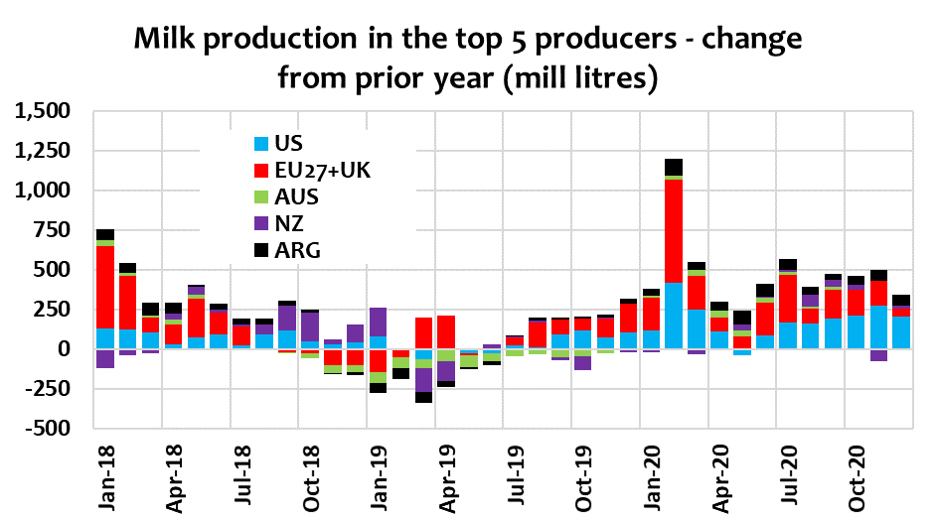

The excess of US milk won’t ease quickly with a continuing build in the herd and improving in farm margins, but cheese and butterfat balance sheets will continue to improve as demand from dining-out and ice-cream producers improves.

The shifting demand between consumption channels across cheese types and formats in the US will continue as a complex developing story, given the regional milk growth patterns. This will have an important bearing on competitiveness between cheese exporters. US cheese futures point to tightening availability.

Feed prices have generally eased a little but remain elevated and will continue to limit northern hemisphere milk growth into H2-2021 with several lingering weather threats in the Americas and eastern Europe.

On the demand side, elevated commodity prices for fats and WMP will further test demand in most developing regions, where weakness is already evident, but firm protein and fat prices won’t let WMP fall too far.

Recent trade data looks flattering given weak comparatives and considering the strong gains in prices since those shipments were booked.

Chinese demand which has dominated recent trade trends continues to hold the key as its internal market reshapes, drawing more ingredients, fats and cheese.

By Dustin Boughton, Procurement Director, Maxum Foods – Your partner in dairy