Global Dairy Commodity Update December 2024

A volatile geopolitical environment and the policy agenda of the US president-elect are overlaying the outlook for global dairy markets.

The acutely tight EU butterfat market remains a major influence, but that will come undone in the short-term as seasonal availability of milk and cream increases, while the direction beyond is uncertain.

The EU milk supply outlook is complex and varied across regions. Elevated milk prices offer better farm margins, but disease and stiffening environmental restrictions may limit a supply response through H1-2025. Milk output is growing in other regions, and milk use is being carefully managed. NZ milk output was up 5% for the season through the peak month, while lower global WMP demand ensures elevated SMP and butterfat output. The full-season outcome is heavily weather-dependent, but expected record milk prices, reduced interest rates and abundant feed supplies will spur producer confidence.

US milk will grow faster in the first half of 2025 with attractive margins and an expanding herd to support additional cheese capacity that is already rolling out. With additional US supplies, global cheese prices will come under pressure as export competition intensifies. While EU cheese prices will ease, exports are critical to internal market balance. US cheese output will grow faster than domestic consumption, while NZ cheese output will also lift.

China’s efforts to stimulate spending and rebalance the dairy supply chain is a critical demand-side variable. Recovery in ingredient imports is expected to be slow after a stock rundown. Volumes will be impacted by low milk prices and slowing local milk production in response to weak consumer demand.

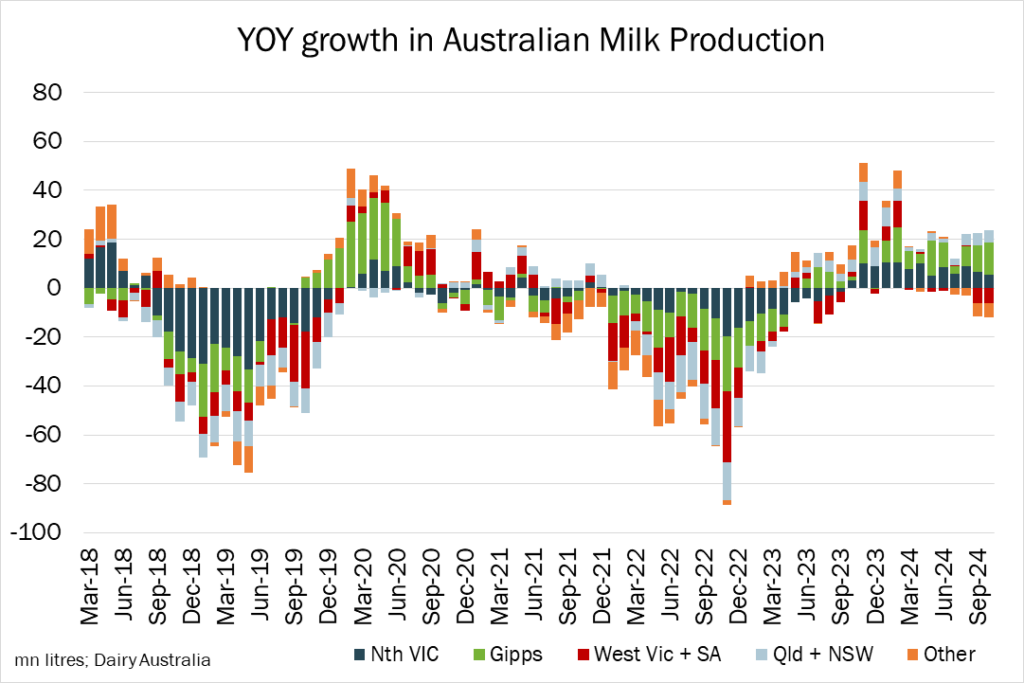

The Australian milk production outlook for the 2024/25 season remained mixed, as dry conditions in West Victoria and Tasmania will limit growth in national output, with excellent conditions in other southern regions. The rainfall outlook for summer has improved however in the latest official outlook.

The Australian full season forecast remains down 1.3% in milk solids (with H1-25 down 2.4%), with the prospect of increased H1-25 farm exits. Australian manufacturing output is expected to move a little towards SMP/butterfat in the current season due to good stream returns.

The local butterfat market is benefitting from high New Zealand prices which in turn are responding to a sustained tight European market. NZ GDT demand has remained robust despite prices rising well above historical tolerance levels.

Cheese sales exposed to commodity conditions will be under increasing pressure as higher US output rolls out. Domestic US demand is unlikely to be sufficient to absorb increased product, and US exporters will be seeking to win share in contestable markets such as Australia. NZ producers are also increasing cheese output in this season. Contracted cream rates through H1-25 remain high and may rise further if butter and AMF remain elevated and milk supply tightens in Q1-25.

By Edwin Lloyd, Executive General Manager – Foods

Ph: +61 7 3246 7810

edwin@maxumfoods.com

Graph Reference: Fresh Agenda