Dairy markets have reacted negatively to supply chain disruption and the fears of weaker demand due to the rapid spreading of coronavirus or COVID-19 outside China. The responses of China and other governments to contain the disease and limit the movement of people have impacted consumer spending in China, and severely disrupted milk flows, processing and land and sea logistics. However, uncertainty grows as we are now in the early stages of a global pandemic, rippling into several regions. The impacts on consumer demand, trade flows and product mix are impossible to forecast with any confidence.

The risk of contracting the disease will change the way people shop, whether they eat out, as well as how milk and ingredients reach processors and retailers. Demand impacts are inevitable in affected regions. In the background, the underlying fundamentals of the global market remain relatively positive. The tight balance in dairy markets might ease with improving growth in milk supply.

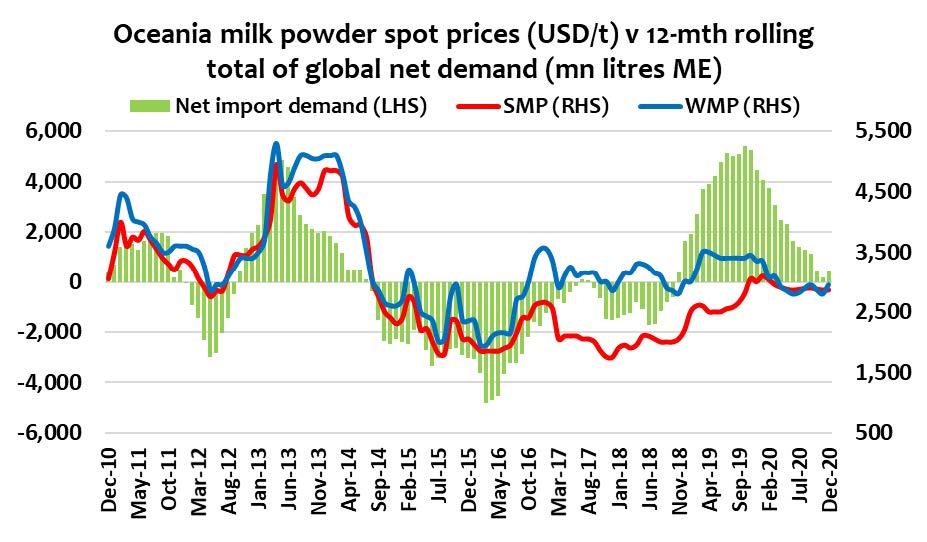

SKIM MILK POWDER

Spot and futures prices weakened by spread of COVID-19, shipping disruptions causing stock-builds. Average shipped prices continued to steadily improve in December. Global trade in the December quarter was 6.1% weaker against high 2018 comparatives. With the December fall, the moving annual tonnage fell 1.7% below peak SMP trade of 2,491mt reached in September.

WHOLE MILK POWDER

European spot values softened in February while NZ prices recovered, tightening the gap between prices. Shipped prices improved month-on-month overall and across all major suppliers. NZ was still at a premium relative to South America.

CHEESE

NZ prices firm with improved demand and SMP/butter returns. EU and US market significantly below Oceania spot/GDT prices. The growth in global cheese trade remained steady at close to 3%, excluding the effect of sales by Belarus to Russia.

BUTTER

EU demand has recovered, steadying prices. NZ spot prices are fragile with price-sensitive Asian market. The US market is weaker with improved milk production and ample cream supplies. While butter has continued to find better traction in SE Asia, China and MENA, AMF trade continued to shrink –trends have worsened in the past 6 months and continued in January with NZ shipments down 20%.

WHEY

EU spot prices rose slightly in January, steadying through February at US$900/t. US prices continues to firm since the start of the year. The decline in global trade in whey products in 2019 was 5.4%, mostly the result of weaker shipments into China & HK which imported 24% less, due to the culling of their pig herd to address swine fever and the imposition of punitive tariffs against US products.

By Dustin Boughton, Procurement, Maxum Foods – Your partner in dairy

Graph Reference: Fresh Agenda