The outlook for global dairy markets through the coming quarters is strongly influenced by tightening milk supplies and remains supportive of high commodity prices.

There are already tight fat and protein supplies in EU and NZ. A slowing in US production is evident, although it will likely remain ahead of prior year comparatives for some time. Northern hemisphere milk production will grow at a slower rate and there are now risks that NZ milk supply may be slowed by cool and wet conditions.

Despite the slow recovery from the economic effects of COVID in some key developing markets, difficult and costly supply chain logistics, and the rising risks that cost inflation will be passed to consumers, dairy demand continues to expand.

Retail demand for dairy products in the domestic markets of the EU and US continues to provide the cushion from COVID’s impacts. As vaccination coverage gradually increases, food service channels will continue to recover as new rules for living with COVID become habit. There is a risk that the damage to household incomes and rising costs of living will affect affordability, while slower retail trade may weaken overall demand in Europe and other regions.

Ignoring the slump in EU-UK trade, global trade continued to grow at moderate pace through July-2021 despite rising commodity prices. Trade has been dominated by the surge in demand due to China’s expanding dairy appetite – growing much faster than local supply – despite its cautious reopening. Demand will likely slow from recent peaks and domestic milk supply will increase, but a large import dependence to provide food security is projected to continue.

Demand from other developing regions is patchy – mostly positive across Sth East Asia, but price-sensitivity has been evident at recent elevated prices in Africa and the Middle East.

By Edwin Lloyd, General Manager Commercial, Maxum Foods – Your partner in dairy

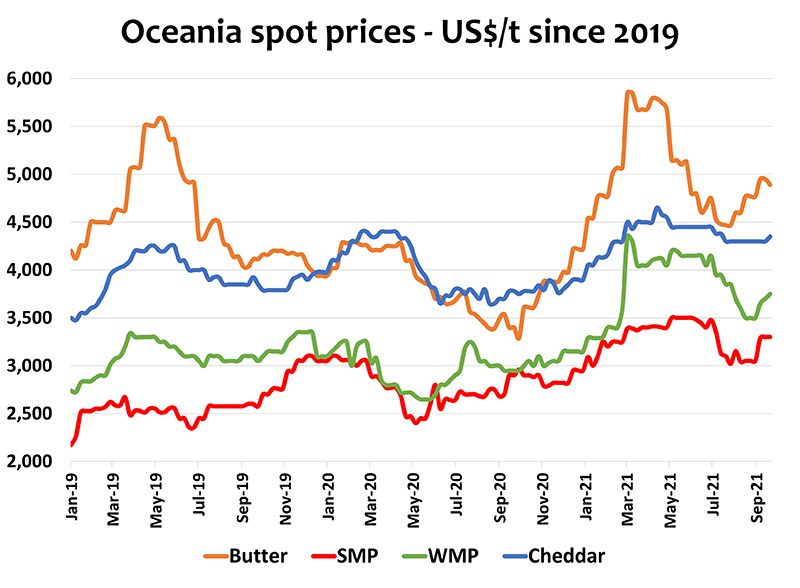

Graph Reference: Fresh Agenda