Global Dairy Commodity Update January 2025

An increasingly complex geopolitical environment and the protectionist agenda of the incoming US president present further risks to the stability of global dairy markets.

The EU butterfat market has weakened with improving seasonal availability of milk, but the direction into Q1-2025 remains uncertain. The EU milk supply landscape varies, as some regions will see a supply response to attractive farm margins, but disease and environmental restrictions may limit a supply response through H1-2025. EU domestic cheese prices are easing with improving milk supplies, resistance to high prices and sluggish demand for EU protein.

US milk production is being curbed in the short-term by a serious disease outbreak in California before strong herd expansions will spur growth in H1-2025 to support increasing cheese capacity. US cheddar output ahead of a demand recovery will weaken fundamental values.

NZ milk output growth is slowing post-peak but now runs into summer weather vagaries. Output in the coming months is heavily weather-dependent, but good feed supplies, record milk prices and reduced interest rates will likely sustain small year-on-year growth.

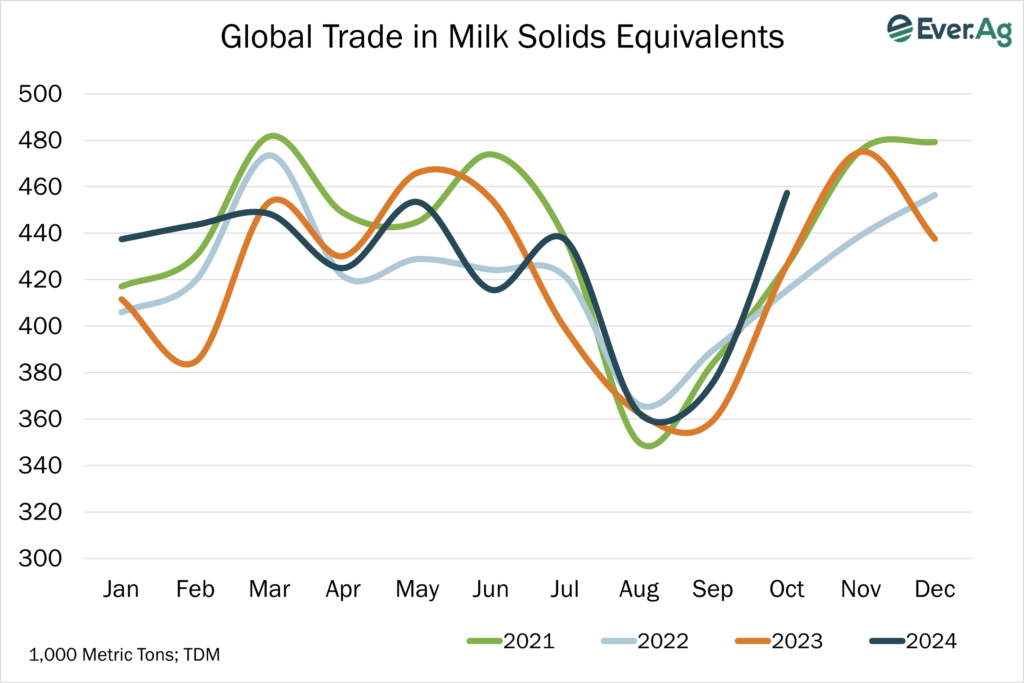

With the outlook for continued reductions in SMP output in the EU and US, the ability for NZ to grow its commodity protein trade and/or improve high-value protein sales remains a fine balancing act. Elevated butterfat output will meet sluggish growth in developing markets.

Cheese market competition in contested markets will remain intense, with growing US supplies, increasing NZ output, and a delicate EU market.

The Australian milk production outlook for the 2024/25 season has improved a little, as widespread rain has improved pasture conditions. Rainfall is likely to be above average over much of southern South Australia, western Victoria, eastern New South Wales and Queensland. In terms of animal feed, grain prices remain below the 5-year average with adequate global supplies and a large domestic grain crop, but fodder prices remain elevated and are likely to be bid higher given pasture conditions. So Australian dairy commodity prices are likely to remain firm for the near future.

By Edwin Lloyd, Executive General Manager – Foods

Ph: +61 7 3246 7810

edwin@maxumfoods.com

Graph Reference: Fresh Agenda