Global Dairy Commodity Update March 2025

Market conditions across major producers are diverse.

EU milk supplies remain under pressure with disease limiting cow numbers and milk growth, despite good conditions and margins in some regions. While output builds seasonally, it is increasingly unlikely milk will expand YOY through the spring flush. Fat and cheese prices have again firmed but the outlook is uncertain, heavily dependent on spring pasture conditions which will support higher commodity output in some regions.

Late-season NZ milk output is under pressure due to drought, but this won’t make a material difference to product supplies. While high-protein demand has limited the exposure to a delicate SMP market, abundant AMF will find traction at an increasingly heavy discount to butter in developing markets.

The US market is struggling in a butterfat glut alongside a fragile cheese market as new plant capacity fills. While limits on young cattle constrain milk growth in H1-25, increased output from new capacity will ensure ongoing volatility in the cheese market. Cheese trade with key contested markets will remain critical to both US and EU producers.

There are a few signs of a rebalancing of China’s supply chain – mostly due to weaker milk output. However meaningful growth in UHT milk and ingredient demand is not yet apparent.

Australian milk output in southern regions continues to slow. Milk output in southern regions worsened in January due to dry conditions which will remain a challenge based on the climate outlook.

Our full season outlook worsened to be down 0.3% in milk solids (H1-25 down 2.3%), with the prospect of increased H1-25 farm exits.

Several companies stepped up milk prices in late Feb-25 with milk values remaining favorable. Milk prices for the 2025-26 season are now coming into focus and are likely to be in the A$9-9.40/kgms range based on the outlook for product values.

Australian trade continues to expand, up 27.5% YOY in December, in milk solids equivalent terms. Export volumes have increased YOY in every month since December 2023.

By Edwin Lloyd, Executive General Manager – Foods

Ph: +61 7 3246 7810

edwin@maxumfoods.com

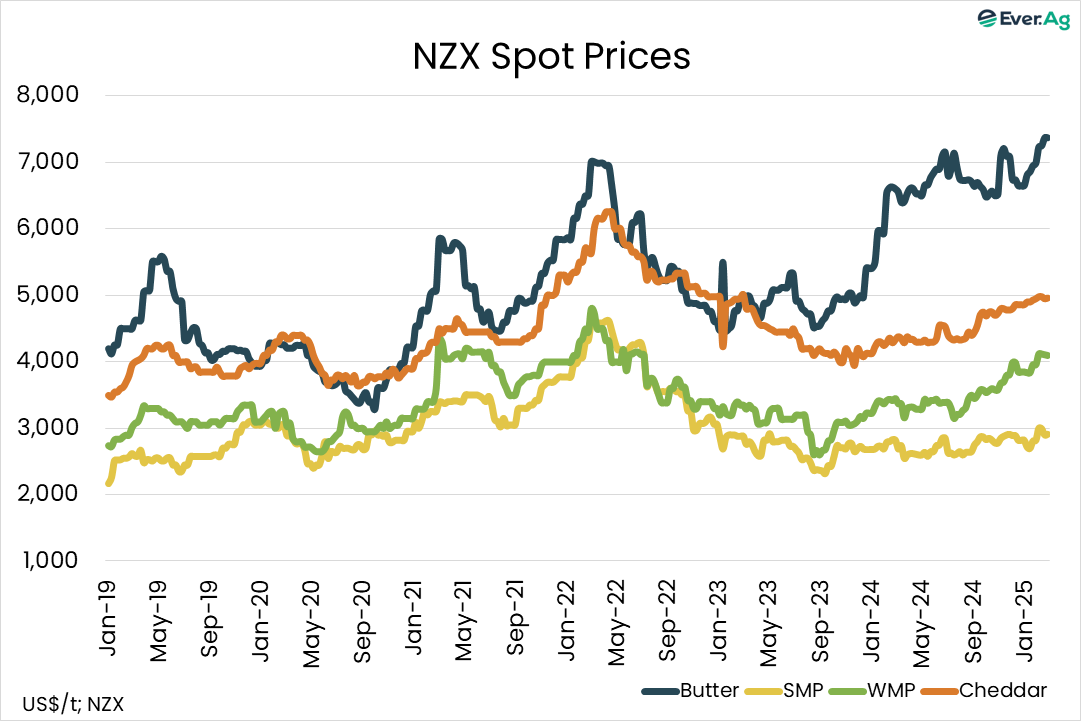

Graph Reference: Fresh Agenda

To view PDF of this release, click here.